Contributed by ICCIE Board Member and Instructor, Carl Terzer of Capvisor Associates

Most Captive Insurers are predominantly bond investors. Since insurers have claims liabilities that must be paid, the bulk of their portfolios consist of high quality, investment grade bonds. These bonds have relatively stable market values as compared to other asset classes, such as equities, making them a more reliable source of funds to pay claims. For example, US investment grade bonds, as measured by the Bloomberg Barclays Aggregate (AGG) index, have had positive returns in 35 of the last 38 years. The stability of these returns can be seen by the fact that the lowest annualized return over that period was -2.92% in 1994. The average annualized return since 1980 is 7.87%, notwithstanding the more recent period of significantly lower returns. These returns, along with the general stability of investment grade bond values, make this asset class the ideal ballast for insurance company “reserve” portfolios.

The problem with bonds is that they have had poor returns for many years, particularly since the great recession. These low returns are predominantly due to intentional market manipulation by the Federal Reserve’s rate, and other monetary, policies. Their zero- to- very low interest rate policies were put into place to provide liquidity to the securities markets with the goal of 1) shortening and shallowing the great recession of 2008 and 2) enabling the economy to grow its way back to health. The AGG’s average annualized return from 1980 to 1987 was 9.25%, a return that could propel an insurer’s growth and be complemented by higher returns from “risk” asset classes like stocks.

From 2008 to 2017 the AGG’s annual return averaged a meager 4.05%. Given an average inflation rate of 1.69% over this period, bond investors experienced average “real” rates of return of 2.36%. With an average inflation rate of 3.85% between 1980 and 2007, investors were much better off with bond investments as they produced a real rate of return of 5.4%.

This low return environment, on both a nominal and real basis, has been a result of the Fed’s easy money policies which reward risk assets, such as equities, over the unattractive returns offered by bonds. And, barring a recession or other market trauma that would cause a flight to safe haven assets like bonds, the future for bond portfolios doesn’t look much better.

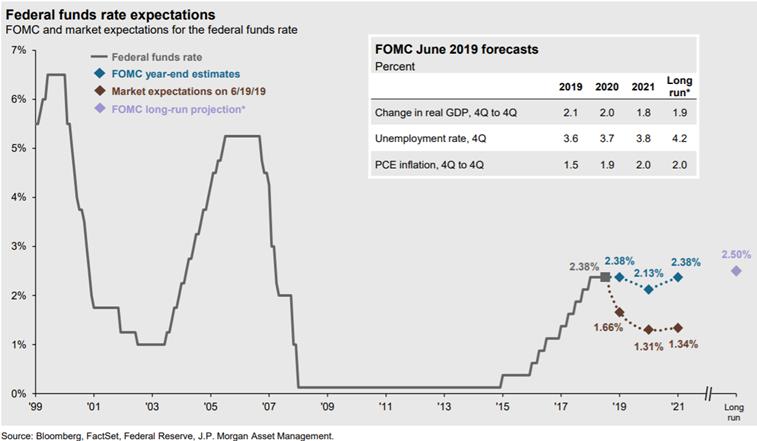

The graph above indicates that there is a serious disconnect between where the Fed and the bond markets think rates should heading. The Fed seeks a rate at equilibrium, the rate at which interest rates neither add nor detract from economic growth. The market thinks that the Fed has already raised rates too far, too fast, which recently has caused a part of the yield curve to invert. Yield curve inversions have been a fairly reliable signal for an upcoming recession. Perhaps in recognition of this, the Fed has recently indicated that they will not be raising rates for the foreseeable future, abandoning their original plan for three more rate increases in 2019 and at least one in early 2020. The bond market did not share the Fed’s rosy view of the economy which has been more evident this year as the US, along with major global economies, have slowed down GDP growth rates.

The bond market seems to have been correct in their assessment of economic strength and we could expect the rates to track a bit closer to the levels the market expects rather than those the Fed projects. In fact, the bond market has already priced in three upcoming rate decreases.

Captive insurers must stick to their guns by using investment grade bond portfolios to serve as the foundation to support their claims-paying ability. They should avoid the temptation to add duration risk to these portfolios and only consider additional credit risk when their financial strength and demonstrated underwriting results can comfortably support that additional risk. Therefore, they will generally be stuck with very low returns from a historical perspective. However, this may mean that it is time to reassess management of bond portfolios to assure that they are getting the greatest return commensurate with the risk level assumed within the bond portfolio. In other words, optimizing bond portfolio performance under current and expected conditions will be extremely important. Risk-adjusted returns should be considered as opposed to nominal returns to best understand the “skill” level of the manager, i.e. how much return per unit of risk? Additionally, captives should optimize their overall asset allocations to take advantage of the strong returns in risk assets to offset the low bond returns. Analytic systems can be helpful to correlate the investment risk with the underwriting risk to optimize the performance of captive portfolios.